Contents

Chapter 4: The Saudi Arabia Economy

4.3 The Tenth Development Plans

Chapter 4: The Saudi Arabia Economy

Saudi Arabia is one of the most oil rich countries in the world, and the largest oil producer. The country took advantage of the competitiveness of the international market for oil, and received extremely high revenues for over 40 years. As such, the oil industry is considered to be the main engine of the country’s economic development (Albassam, 2015). Since the 1980s, the industry has contributed to half of the total Gross Domestic Product (GDP), according to the Central Department of Statistics and Information of Saudi Arabia. Although the oil industry has contributed significantly to the economic development in Saudi, relying on it has created a major problem for the economy. The non-diversified economy that has emerged has resulted in unsustainable development and a weak private sector, which contributed 10% to total GDP between 2004 and 2013 (Aldarwish et al., 2015).

Additionally, the private sector could not generate high-skilled job opportunities. Instead, the majority of job opportunities in the private sector are low-skilled and low-wage jobs that has resulted in an increase of foreign workers in this sector of up to 50% (Khorsheed et al., 2014). As around 57% of job seekers in Saudi are highly educated, they refuse to take these low-skilled jobs that do not require high academic qualifications. In addition, the private sector does not provide the necessary training programs to enhance skills and productivity to engage the local workers to the private sector (De Bel-Air, 2014). Consequently, diversifying the economy is necessary to decrease the risk of volatility and uncertainties in the international oil market that could cause problems for the economy (Walker, 2015), and to help generate suitable job opportunities in the private sector. Furthermore, a diversified economy would assist in achieving sustainable growth away from the oil industry through strengthened productivity and contribution of the private sector (Aldarwish et al., 2015).

The Saudi government have adopted policies to strengthen private sector and achieve diversification by enhance the business environment and to reform the labour market to increase the employment rate in different development plans have been issued, with the latest covering 2015-2019 (Albassam, 2015). Economic diversification has been a main target of the government in all 10-development plans, according to the Saudi Arabian government’s first development plan (1970-1975), one of three objectives was: “diversifying sources of national income and reducing dependence on oil by increasing of other productive sectors in gross domestic product” (Ministry of Economy and Planning, 2014, p.23). Even though economic diversification has been the main goal of development plans in Saudi Arabia since 1970, the result of the current analysis shows that the oil sector remains the engine driving the economy. Many reasons have been suggested to explain the government’s lack of success in diversifying the economy. Among them there are the absence of clear plan that addresses in detail the process of diversifying the economy, the government support provided to industries that are profoundly dependent on oil (e.g., petrochemical industries), the almost complete dependence of the private sector on government spending and projects, and lack of clear and specific plan support non-oil sectors (agriculture, service).

This chapter is organised as follows. First, a review of the Saudi economy, where the main features of the Saudi economy are discussed, in addition to brief outline of the main objectives of all ten Development plans. Second, the 10th Development plan (2015-2019) is discussed in term of the main features and the main issues in the Saudi economy, as well as explain entrepreneurship ecosystem in Saudi and what need to be done to support entrepreneurship and SMEs. Finally, an outlook of research case study the National Entrepreneurship Institute (NEI) and explain in more details the main programs of NEI to support entrepreneurship and SMEs.

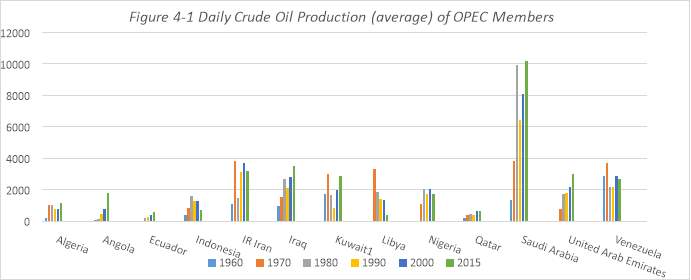

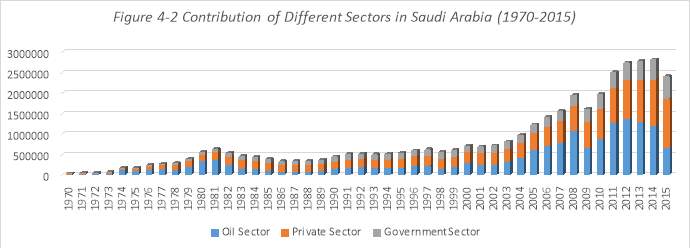

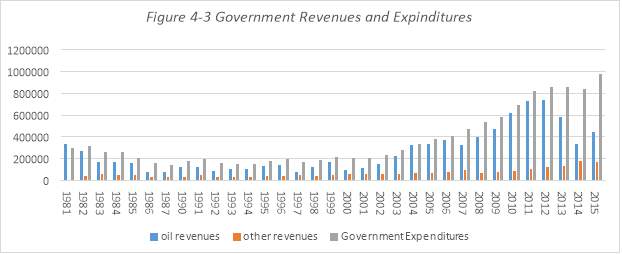

Saudi Arabia is one of the most oil rich countries in the world, and the largest oil producer, see Figure 4-1 the daily crude oil production (average) of OPEC members for the last 6 decades. Comparing with other members of OPEC, Saudi Arabia is considered the largest oil producer since 1970s, since it has the highest average of the daily crude oil production. The country took advantage of the competitiveness of the international market for oil, and received extremely high revenues for over 40 years. As such, the oil industry is considered to be the main engine of the country’s economic development (Albassam, 2015). Since the 1970s, the oil sector has contributed significantly to the total Gross Domestic Product (GDP), see Figure 4-2 contribution of different sectors to the GDP in Saudi Arabia (1970-2015). In addition, the Saudi government has relied mainly on the oil revenues to cover all the government expenditures since the 1980s, see Figure 4-3 Government revenues and expenditures. The main government expenditures cover the following:

- Human resource development;

- Transport and communication;

- Economic resource development;

- Health and social development;

- Infrastructure development;

- Municipal services;

- Defence and security;

- Public administration and other government spending; and

Government lending institutions.

Government lending institutions.

Source: OPEC Annual Statistical Bulletin Report, 2016.

Source: OPEC Annual Statistical Bulletin Report, 2016.

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Note: data for 1989, 1990 and 1991 are not available.

Although oil industry has contributed significantly to the economic development in Saudi since it contributes significantly to the GDP and it covers all the government expenditures, relying on it has created a major problem for the economy. The non-diversified economy that has emerged has resulted in unsustainable development, meaning any changes in the oil prices would impact directly on the Saudi economy, and this is what happen recently in 2015 that has resulted to major changes in the Saudi economy and policy. To explain, when the oil prices fall significantly in 2015 to reach 46.47 US $ per barrel, see Table 4-1 changes in oil prices, the oil revenues decreased and the GDP decreased as well since the oil sector’s contribution to the GDP decreased in 2015, see Figure 4-2 and 4-3.

Table 4-1 Changes in Oil prices (Arabian Light), Nominal and Real Prices

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Oil Prices of the Arabian Light | ||||||||||

| Nominal Price (*) | 61.10 | 68.75 | 95.16 | 61.38 | 77.82 | 107.82 | 110.22 | 106.53 | 97.18 | 49.85 |

| Real Price (*) | 59.94 | 62.59 | 80.38 | 53.89 | 68.60 | 88.79 | 93.06 | 88.95 | 80.34 | 46.47 |

Source: the Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

(*) Base year 2005, and the prices in US$ per Barrel.

Theoretically, changes in oil prices are expected to have two contradictory effects on the private sector and manufacturing sector, since the production cost will reduce. However, this is not the case in Saudi Arabia, where the government plays an important role in supporting manufacturing and private sector and relying on the oil export revenues in their support. Therefore, lower oil price will reduce export revenues, and the government may not be able to provide the same level of support to privet and manufacturing sector as it used to do (Mahboub and Ahmad, 2017). This has led to adopt new changes in the Saudi economy and policy such as decreasing the government expenditures for 2016 in education and militarily sectors, as well as announcing the 2030 vision in 2016 during an interview with Prince Mohammed Bin Salman.

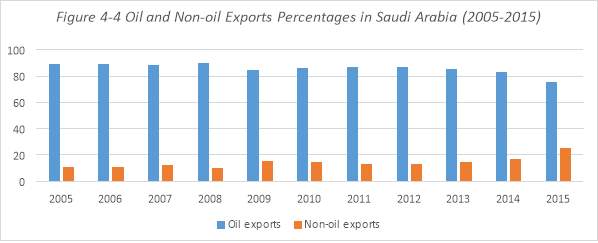

In term of diversification, Saudi Arabia needs economic diversification for at least four reasons. First, it would reduce the exposure of the economy to volatility and uncertainties in the global oil market. Second, it would help create jobs in the private sector that are needed to absorb the young and growing working-age populations into the workforce. Third, it would help increase productivity and sustainable growth. Fourth, it would help put in place the non-oil economy that will be needed many years down the road when the oil revenues start to decrease (Al-Darwish et al., 2015a). Although Saudi Arabia’s economy has evolved significantly over the past decade, as seen in Figure 4-2 the contributions of different sectors to GDP, further diversification is important to avoid risks in one-sided heavy reliance on production and export. Figure 4-4 indicates the heavy reliance on the oil exports with almost 90% in 2005, which decreased slightly during the following years to around 73% in 2015.

🌐

Studying abroad? We know your country's system.

UK student? We use OSCOLA, Harvard, or Vancouver. US college? APA 7th or Chicago. Australian? We know APA 6th, AGLC, and more. One platform, global expertise.

Serving students in 70+ countries

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Saudi Arabia compares relatively well across several business indicators, yet challenges remain. For instance, the country has been doing well in terms of its business and infrastructure, incentives for export promotion, labour market regulation, and education. However, challenges remain in contract enforcement and resolution of company insolvencies, and in trade integration, despite export incentives (Al-Darwish et al., 2015a). In term of business climate, Saudi Arabia was ranked as the 29th most competitive economy worldwide among 138 countries according to the Global Competitive Index 2016-2017 (Schwab, 2017). Global Competitiveness Index combines 114 indicators that capture concepts that matter for productivity and long-term prosperity. These indicators are grouped into 12 pillars, these pillars are in turn organised into three groups (basic requirements, efficiency enhancers, and innovation and sophistication factors):

- Factor-driven economies: institutions, infrastructure, macroeconomic environment, health and primary education.

- Efficiency-driven economies: higher education and training, goods market efficiency, labour market efficiency, financial market development, technological readiness and market size.

- Innovation-driven economies: innovation and sophistication factors.

Figure 4-5 shows the Global competitiveness rank in three countries of the Gulf Cooperation Council (GCC), these are United Arab Emirates, Qatar and Saudi Arabia. According to this report, Saudi Arabia comes at 29th, losing four places mainly because of a deteriorating macroeconomic environment following the drop-in oil prices. In details, in the basic requirements, the macroeconomic environment has the lowest rank (68); in the efficiency-driven economies, the lowest rank was in the labour market efficiency; and in the innovation-driven economies, the innovation is the lowest rank. Therefore, achieving higher diversification will require enhancing the macroeconomic environment to the basic requirements, building capacities in innovative industries and services sectors to enhance innovation and sophistication factors. Strengthening education, will be necessary, but also will be a more flexible labour market that ensures that talent is used efficiently (Schwab, 2017).(Jeddah-Chamber, 2016)

Source: Global Competitiveness Report, 2016- 2017.

Insufficient labour market can be explained by four of the main challenges in Saudi Arabia. First, a lack of competitive and fulfilling private sector jobs attractive to Saudi nationals, since the majority of job opportunities in the private sector are lower-skilled and low-wages jobs that has resulted in an increase of foreign workers in this sector up to 50% (Khorsheed et al., 2014). As around 57% of job seekers in Saudi are highly educated, they refuse to take these low-skilled jobs that do not require high academic qualifications. In addition, the private sector does not provide the necessary training programs to enhance skills and productivity to engage the local workers to the private sector (De Bel-Air, 2014).

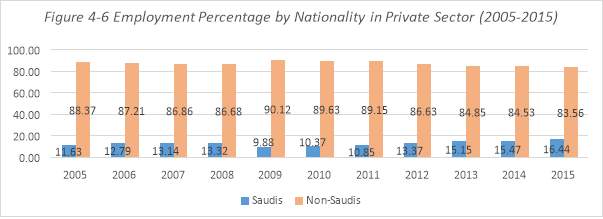

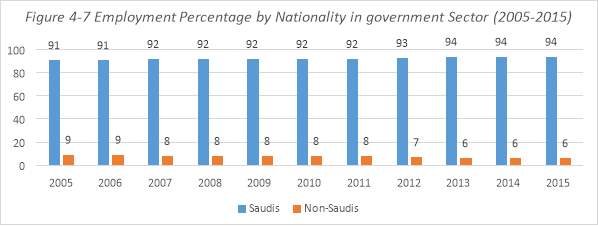

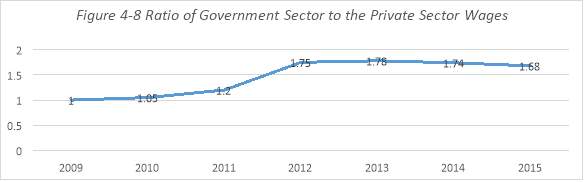

In addition, state-owned enterprises still provide most of the jobs for Saudis entering the workforce, with about two-thirds of Saudis employed in the public sector. Expanded opportunities within the private sector have not changed perceptions of these jobs. Saudi nationals continue to view public-sector work as more attractive than private employment. As a result, private sector jobs are overwhelmingly held by expatriates, as shown in Figure 4-6 while Saudis dominate the public-sector job market in Figure 4-7. As Figure 4-8 shows, the ratio of government sector to private sector wages is changing slightly, but still the government sector wages are better than private sector wages, which reinforces many Saudis’ employment perceptions. In addition, many public-sector jobs require a work week of 40 hours or less, while private sector jobs often demand six days and more than 50 hours each week. Accordingly, younger workers often prefer to stay jobless and wait for public sector vacancy. Therefore, although the number of Saudis in the private sector has been increasing, the private sector mainly relies on foreign labour, which is considered the second challenge in the labour market (MOL, 2016).

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016).

Source: Saudi Arabian Monetary Authority (SAMA), Annual Statistics (SAMA, 2016)

Source: Manpower & Employment, Talent Management, and Compensation, 2016 by Jeddah Chamber.

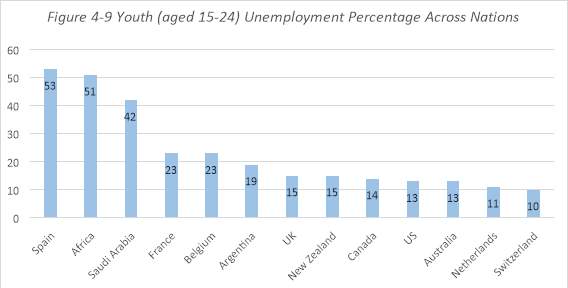

Third challenge is youth unemployment in Saudi Arabia, as annually, numerous Saudis join the workforce, but the youth of the nation is still largely unemployed. Although the total youth unemployment in 2014 was 30%, the youth unemployment among Saudis stood high as 42%. Comparing the unemployment by youth group (15-24), Saudi Arabia has a significant percentage of youth unemployment, see Figure 4-9. A major driver of the high unemployment rate is the substantial disparity between the skill set of youths and the skills required by the private sector. Thus, it is important for the government to take initiatives, to manage the expectations of its youth population by providing support in the form of training and mentorship. Additionally, improving job security and working conditions, implementing strategies to create more competitive, and fulfilling jobs, along with higher wages, would also help in making the private sector more attractive for the youth in Saudi Arabia (Jeddah-Chamber, 2016).

Source: Saudi Arabia- Manpower and Employment Talent Management and Compensation Report, by Jeddah Chamber (2016).

Saudi Arabia- Manpower and Employment Talent Management and Compensation Report, by Jeddah Chamber (2016).

Fourth, demand for labour is not being efficiently matches with the supply of labour, meaning mismatch between demand and supply especially in connecting jobs seekers to opportunities that most effectively match their skills, is considered another obstacle in the labour market in Saudi Arabia. The link between job seekers and private employers is clearly not functioning effectively. Part of the reason for lack of publicly available information is that labour market has traditionally relied on personal connections and networks (MOL, 2016, Jeddah-Chamber, 2016). Based on survey results done by Oxford Strategic Consulting of Saudi employment, not having good contacts is considered one on the significant difficulties Saudis face in finding jobs (Najat et al., 2016)

The Saudi government has adopted several development policies considering these issues within the last 10 development plans, see Table 4-2 (4 parts) for more details on the objectives of all 10 development plans, where it is obvious that diversification, employment and strengthen the private sectors are considered since the first development plan. The following section discuss the policies to tackle the fundamental issues in the Saudi economy, by focusing more on the 10th development plan (2015-2019).

Table 4-2 the 10 Economic Development Plans of Saudi Arabia (Part 1)

| Plan Name | Framework Time | Objectives |

| 1st Development Plan | 1970-1974 |

|

| 2nd Development Plan | 1975-1979 |

|

| 3rd Development Plan | 1980-1984 |

|

Source: Ministry of Economy and Planning of Saudi Arabia, 1st, 2nd, and 3rd development plans.

Table 4-2 the 10 Economic Development Plans of Saudi Arabia (Part 2)

| Plan Name | Framework Time | Objectives |

| 4th Development Plan | 1985-1989 |

|

Source: Ministry of Economy and Planning of Saudi Arabia, 4th development plan.

Table 4-2 the 10 Economic Development Plans of Saudi Arabia (Part 3)

| Plan Name | Framework Time | Objectives |

| 5th Development Plan | 1990-1994 |

|

| 6th Development Plan |